Overview of the Tax System

Romania's tax system is structured to accommodate various business needs. Here's a quick glance at the key taxes that might be relevant for entrepreneurs and businesses:

| Tax Type | Rate | Notes |

|---|---|---|

| Corporate Tax | 16% on profit or 1% on revenue | 16% on profit for standard companies; 1% on revenue for micro-enterprises with revenue under €500,000 |

| Dividend Tax | 8% | Applicable to dividends distributed to shareholders |

| VAT | 19% (standard rate) | Reduced rates (5% or 9%) for certain goods/services; exemptions for specific activities |

| Property Tax | Varies | Based on property value, location, and usage; specific rates for residential and commercial properties |

Register your Romanian Company

Start a business on the right foot, by registering your business with Incorpo.ro

We help you get access to the banks you require, and guarantee your money back if anything goes wrong!

Chapter 1: Introduction to Romania's Tax Landscape

1.1 The Romanian Tax Environment

Corporate Taxation:

- Standard Profit Tax: Companies in Romania are subject to a 16% tax on profit, a rate that aligns with many European nations.

- Micro-Enterprise Tax: For businesses classified as micro-enterprises with revenue under €500,000, a special 1% tax on revenue applies. This rate aims to support and encourage small business growth.

Value-Added Tax (VAT):

- Standard Rate: The general VAT rate in Romania is 19%.

- Reduced Rates: Certain goods and services, such as food products or cultural events, benefit from reduced VAT rates of 5% or 9%, following specific guidelines.

Property Tax Considerations:

- Variable Rates: Property taxes in Romania range from 0.08% to 1.5%, depending on factors such as the value, location, and function of the property. Residential properties often have lower tax rates compared to commercial properties.

1.2 Regulatory Compliance and Strategic Insights

Legal Framework:

- Compliance Requirements: Romania's legal framework outlines specific compliance requirements, such as periodic filings and adherence to accounting standards.

- R&D Incentives: Businesses engaged in research and development activities can benefit from a 50% additional deduction of eligible R&D expenses, encouraging innovation.

Economic Strategy:

- Supporting Various Business Stages: The differentiated tax rates, such as the 1% revenue tax for micro-enterprises, are part of Romania's strategy to support businesses at different growth stages.

Chapter 2: Key Aspects of the Romanian Tax System

2.1 Corporate Taxation in Detail

Standard Profit Tax:

- Rate: 16% tax on profit for standard companies.

- Applicability: This rate applies to both resident and non-resident companies on their worldwide income, provided they meet specific criteria.

- Filing Requirements: Corporate tax returns are generally due annually, by March 31 of the following year.

Micro-Enterprise Tax:

- Rate: 1% tax on revenue for micro-enterprises with revenue under €500,000.

- Eligibility: Companies with at least one employee and revenue below the threshold qualify.

- Benefits: This simplified tax regime aims to reduce administrative burdens and foster small business growth.

2.2 Dividend Tax Insights

Dividend Tax Rate:

- Rate: 8% on dividends distributed to shareholders.

- Applicability: This rate applies to both individual and corporate recipients.

- Reduction Opportunities: Double taxation treaties may lead to reduced rates for non-residents.

2.3 Understanding Value-Added Tax (VAT)

Standard VAT Rate:

- Rate: 19% is the standard VAT rate in Romania.

- Goods and Services: This rate applies to most goods and services sold in the country.

Reduced VAT Rates:

- 5% Rate: Applies to specific goods like books, newspapers, and certain medical equipment.

- 9% Rate: Applies to hotel accommodation, restaurant services, and certain medical and pharmaceutical products.

Exemptions:

- Examples: Certain activities, such as education and healthcare services, are exempt from VAT in Romania.

2.4 Property Tax Considerations

Property Tax Rates:

- Residential Property: Rates range from 0.08% to 0.2% based on the property's value.

- Commercial Property: Rates range from 0.2% to 1.5%, varying by location and usage.

- Local Regulations: Local authorities may implement specific regulations affecting property tax.

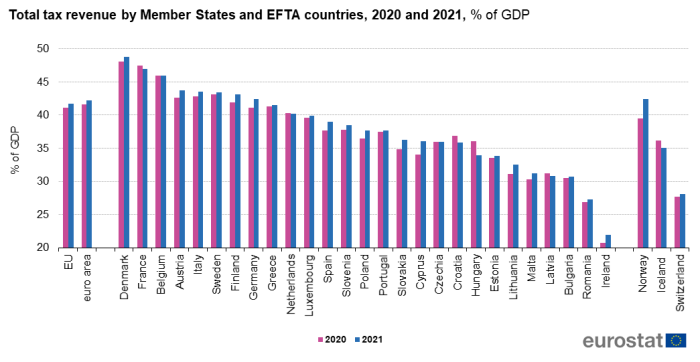

Chapter 3: Romania vs. The World - A Tax Comparison

3.1 Graphs and various other measures of Romanian business registration tax advantages.

3.2 Comparative Analysis with the UK, Delaware, and Bulgaria

Corporate Taxation:

- Romania: 16% on profit or 1% on revenue for micro-enterprises with revenue under €500,000.

- UK: 19% on profit, with plans to increase to 25% for profits over £250,000 by 2023.

- Delaware (USA): No state corporate income tax on goods and services provided by Delaware corporations operating outside of Delaware.

- Bulgaria: 10% on profit, one of the lowest in the European Union.

Dividend Taxation:

- Romania: 8% on dividends.

- UK: Ranges from 7.5% to 38.1% based on income level.

- Delaware (USA)Subject to federal tax rates, ranging from 0% to 20%.

- Bulgaria: 5% on dividends.

Value-Added Tax (VAT):

- Romania: 19% standard rate, with reduced rates of 5% and 9% for specific goods/services.

- UK: 20% standard rate, with reduced rates for certain categories.

- Delaware (USA): No state-level sales tax.

- Bulgaria: 20% standard rate, with reduced rates for specific categories.

Effective Tax Rate Comparison:

- Yearly Revenue Thresholds:

- Romania vs. UK: Romania becomes more advantageous when yearly revenue exceeds €8,286.

- Romania vs. Delaware: Advantageous in Romania for yearly revenue exceeding €10,986. Businesses intending to reach the NYSE are recommended to choose Delaware once they grow over 1.000.000 yearly revenue.

- Romania vs. Bulgaria: Advantageous in Romania for yearly revenue below €500,000 with higher profit margins, with companies making over €500.000 EUR being recommended to register in Bulgaria for a lower tax footprint or consider other jurisdictions that are more fit for growth (e.g., Delaware).

3.3 Insights into Bureaucracy and Other Factors

- Romania: Moderate level of bureaucracy; business-friendly policies for small and medium enterprises.

- UK: Relatively efficient bureaucracy; established legal and business framework.

- Delaware (USA): Known for business-friendly regulations and an efficient legal system.

- Bulgaria: Lower effective tax rate for high revenue companies but higher bureaucracy and administrative costs.